This post compares Tria, Crypto.com, MetaMask Card, Wirex, Gnosis Pay, and Coinbase Card across all three, then runs the real math on what someone spending $2,000 and $5,000 a month earns over a year.

How crypto card cashback actually works

Crypto card cashback is structurally similar to traditional card rewards: a percentage of each transaction is paid back to the cardholder. What differs is the currency you receive and whether you have to commit capital to unlock the higher rates.

Cashback in fiat vs. in tokens vs. in stablecoins

The currency you’re paid in determines whether the cashback rate you see is the cashback rate you keep.

- Fiat cashback — paid back to your card balance in local currency. The number on the screen is what you keep. Few crypto cards offer this directly.

- Stablecoin cashback — paid in USDC, USDT, or another dollar-pegged stablecoin. Functionally close to fiat. Increasingly the default for self-custodial cards in 2026.

- Native-token cashback — paid in the issuer’s own token (Crypto.com’s CRO, Wirex’s WXT, Gnosis Pay’s GNO). Headline rate looks attractive, but realized value depends on the token’s price between when you earn it and when you sell. Often there are also lockup or unstaking periods that delay your access.

The simplest test: if you can’t immediately convert the cashback to dollars at the rate listed, the rate listed is not what you’re earning.

The "tier-locked" trap (when cashback requires holding the issuer's token)

The other quiet condition on most crypto card cashback is tier-locking: the headline rate is only available if you hold (or stake) a certain amount of the issuer’s token. Crypto.com is the canonical example — its highest tier requires staking $400,000+ worth of CRO. MetaMask’s onchain rewards layer ties higher rates to MASK token holding (or activity-based qualifications). Wirex applies tier conditions tied to WXT holdings.

What this means in practice: the cashback you see in the marketing copy is almost always the top-tier rate, available to a small fraction of users. The rate you’ll actually see, with the holding profile most people have, is typically half to a third of the headline. We’ll work this out concretely in the math section below.

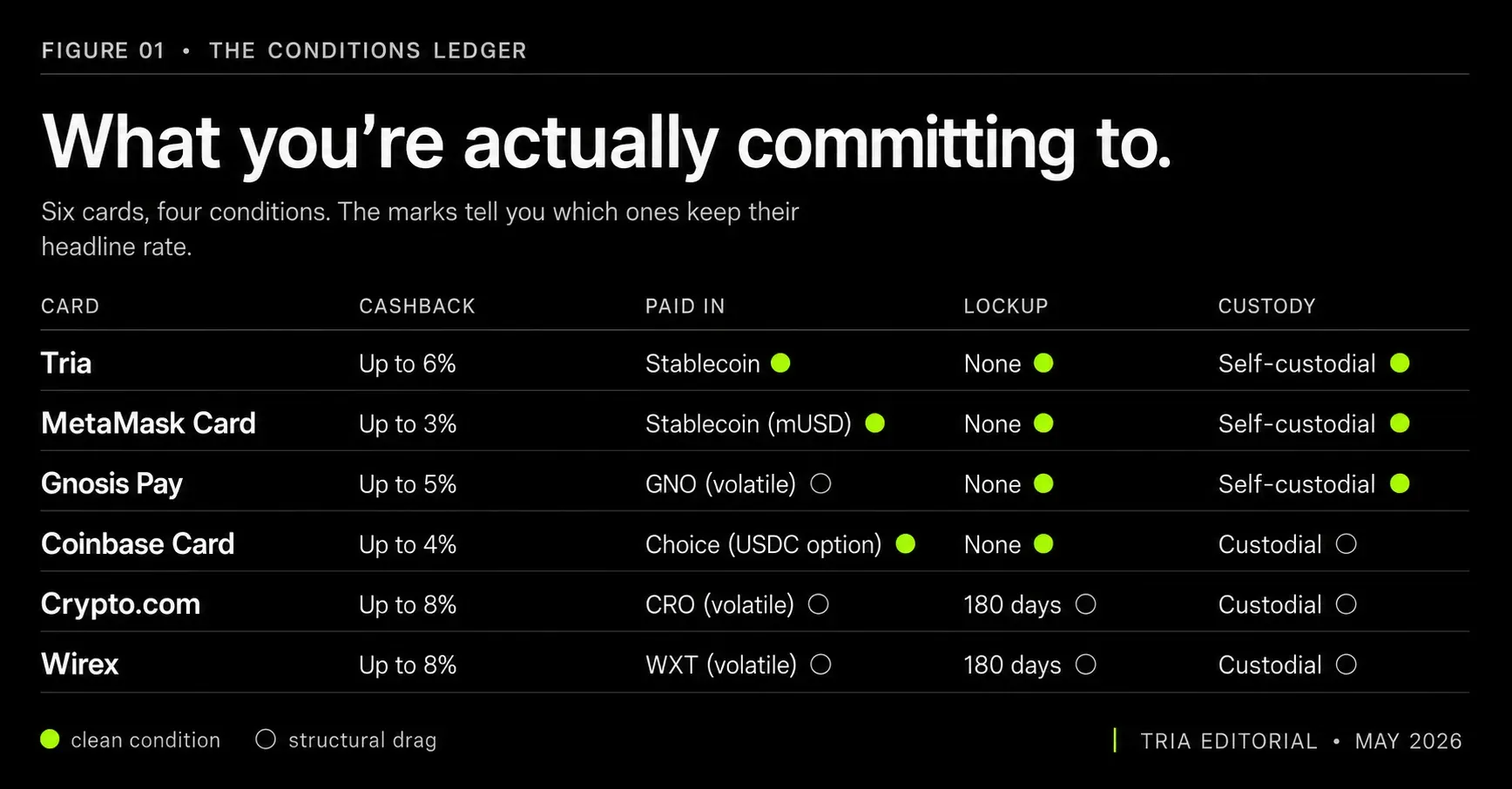

Cashback rates across major crypto cards in 2026

Six cards account for most of the volume in the crypto cashback category in 2026. Below is the honest comparison — including the conditions, not just the headline rates.

Tria Card (up to 6% cashback, paid in stablecoins)

The Tria Card is a self-custodial Visa card linked directly to your Tria balance. Cashback up to 6% is paid in stablecoins to your self-custodial wallet — meaning the rate you see is the rate you keep, with no volatility discount and no waiting period.

Three structural advantages set the Tria Card apart in the cashback category:

- No token to hold. The cashback rate isn’t gated on staking or holding a Tria-issued token. You don’t carry the price risk that other cards bake into their headline rate.

- Stablecoin payout. Cashback is paid in USDC, retained at full value, immediately available — no lockup or unstaking period to wait through.

- Compounding while it waits. The underlying balance keeps earning on-chain yield in Tria’s Earn product (up to 15% APY) until the moment you use the card. That’s a benefit unique to self-custodial real-time cards — your balance does two jobs at once.

Tier structure: Cashback varies by card tier (Virtual, Signature, Premium) and merchant category, with the up-to-6% rate available on the Premium tier for top categories.

Crypto.com Card (tiered, custodial, up to ~8% at top tier)

The Crypto.com Card has been the cashback benchmark in the category since 2021, with rates from 1% (Midnight Blue, no CRO staking) up to roughly 8% (Obsidian, requiring approximately $400,000+ CRO staked for 6 months). Cashback is paid in CRO tokens.

Two important caveats. First, the card is custodial — your balance sits with Crypto.com, not with you. Second, the headline tier numbers have been cut multiple times in the past three years; the rate you sign up for isn’t necessarily the rate you keep. Realistic effective rates for most users sit at the lower tiers (1–3%).

MetaMask Card (US, ~3% in onchain rewards)

MetaMask launched its US Mastercard in early 2026 with onchain rewards in the 1–3% range, paid as redeemable points or wallet-native rewards rather than direct cashback. The card is self-custodial — funds stay in the user’s MetaMask wallet until purchase. Higher tiers are tied to MASK token activity in MetaMask’s broader rewards program.

Wirex (Cryptoback in WXT)

Wirex offers up to ~8% Cryptoback paid in WXT tokens. Like Crypto.com’s CRO model, the headline rate requires WXT staking, and the realized value depends on WXT’s price at the moment you sell. Wirex sits in a transitional category — historically custodial, with self-custody features rolled out gradually.

Gnosis Pay (up to 5% in GNO)

Gnosis Pay is one of the cleanest self-custodial card products in 2026. Cashback up to 5% is paid in GNO tokens, scaled to GNO holdings. The card itself is fully self-custodial via a Safe Smart Account on the Gnosis Chain, which means your assets never leave your wallet. Strong product for DeFi-active users; less convenient for users who don’t want exposure to GNO.

Coinbase Card (1–4%, in a selected asset)

The Coinbase Card pays 1–4% cashback in your choice of supported asset (BTC, ETH, USDC, etc.). The card is custodial — you draw from your Coinbase account balance. Rates have been competitive but unspectacular; the convenience of integration with the broader Coinbase account is the main draw.

The honest math: what would you actually earn?

Headline rates only matter if you take them home. The realistic 12-month payout depends on monthly spend, payment currency, lockup conditions, and the price behavior of any issuer token you receive.

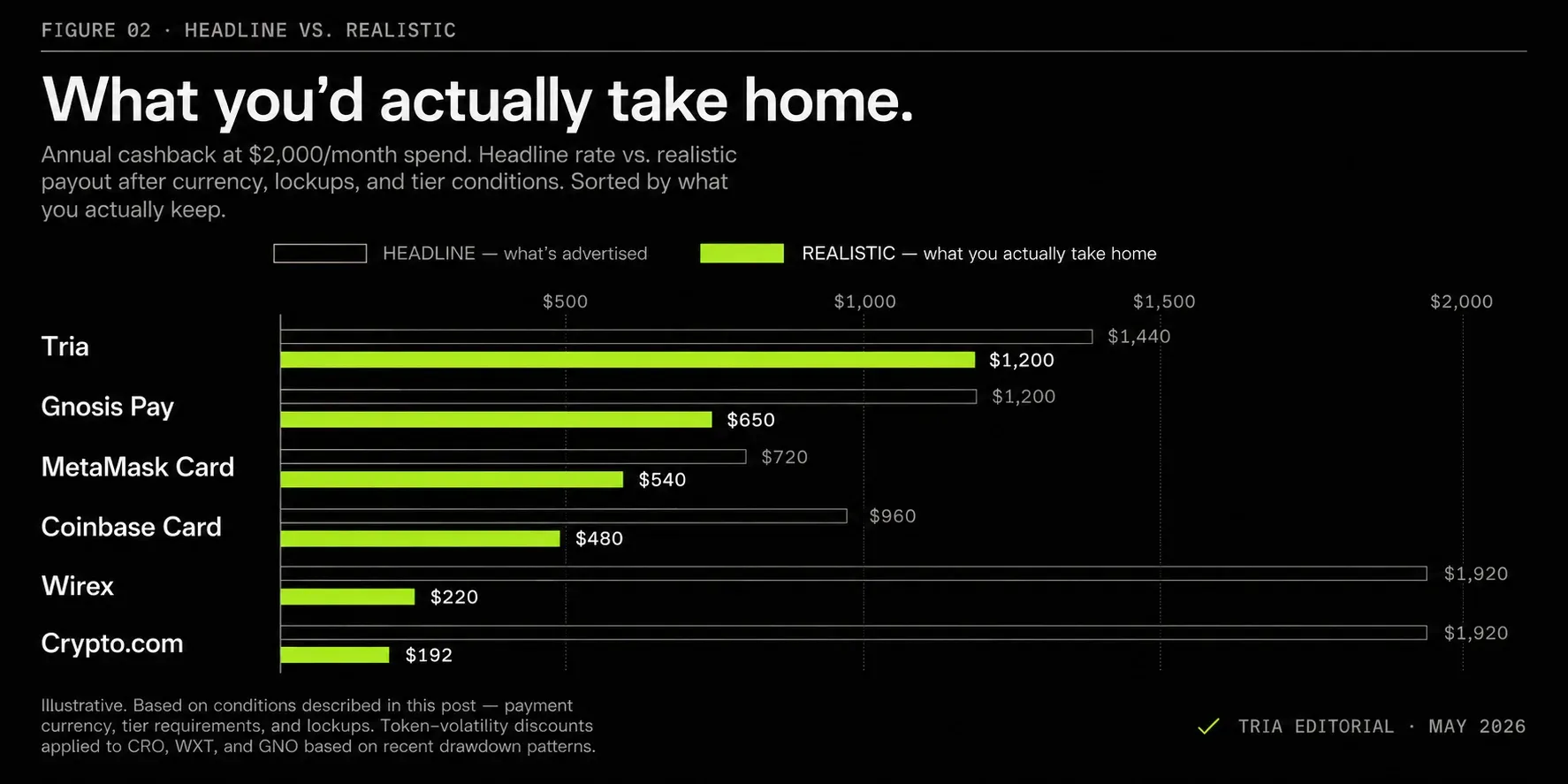

Worked example — $2,000/month spend (typical retail user)

A user spending $2,000/month puts $24,000 through the card over 12 months. Here’s the rough realistic math:

- Tria (up to 6%, paid in stablecoins, no token to hold): ~5% blended rate is realistic for most users (top rate requires Premium tier; Signature tier averages lower). $24,000 × 5% = ~$1,200/year in stablecoins, retained at full value with no lockup.

- Crypto.com (1% no-staking tier): Most users without significant CRO staked sit at the bottom tier. $24,000 × 1% = $240/year in CRO. Apply a 20% volatility discount → ~$192/year realized.

- MetaMask Card US (~3% in onchain rewards): $24,000 × 3% = $720/year. Realized value depends on the MASK token’s behavior; on a conservative basis treat realized as ~$540/year.

- Wirex (1–2% no-staking tier in WXT): $24,000 × 1.5% = $360/year in WXT. WXT has had significant drawdowns; realistic realized closer to ~$220/year.

- Gnosis Pay (~3% mid-tier in GNO): $24,000 × 3% = $720/year in GNO. Apply ~10% volatility discount → ~$650/year realized.

- Coinbase Card (~2% paid in USDC): $24,000 × 2% = ~$480/year, retained at full value.

The takeaway: at $2,000/month spend, Tria’s realistic payout (~$1,200) is roughly 2× the next-best card and 6× the lowest. The reason isn’t a higher headline rate — it’s that stablecoin payment and zero token-staking conditions mean the realized cashback closely tracks the headline.

Worked example — $5,000/month spend (digital nomad / heavy user)

At $5,000/month — roughly the spend pattern of a digital nomad or someone using the card as their primary payment method — the math scales proportionally, and the gap widens:

- Tria (~5% blended, stablecoin, no lockup): $60,000 × 5% = ~$3,000/year.

- Crypto.com (1% no-staking): $60,000 × 1% × 0.8 volatility = ~$480/year.

- MetaMask Card US (~3%): $60,000 × 3% = $1,800/year, realized ~$1,350.

- Wirex (~1.5% no-staking): $60,000 × 1.5% × 0.6 volatility = ~$540/year.

- Gnosis Pay (~3% mid-tier): $60,000 × 3% × 0.9 = ~$1,620/year.

- Coinbase Card (~2%): $60,000 × 2% = ~$1,200/year.

At $5,000/month, Tria’s realistic cashback (~$3,000) clears the next-best card by almost $1,400/year and clears the lowest by roughly $2,500. Add the yield earned on idle balance (up to 15% APY through Tria’s Earn product while the funds wait) and the gap widens further — a benefit no custodial card can offer because their idle balances aren’t yours to begin with.

Why headline cashback rates aren't the full story

Three quiet factors usually account for the gap between headline and reality:

- Tier-locking requires capital you may not want to commit. The top Crypto.com tier requires roughly $400,000 in CRO staked — capital that has its own opportunity cost and price risk separate from the cashback.

- Native-token volatility means the headline rate isn’t the realized rate. A 5% cashback in a token that drops 40% nets you roughly 3%.

- Lockup and unstaking periods delay access to cashback for weeks or months. During that window, you can’t hedge or convert. If the token drops, you’re holding the bag.

Headline rates make for clean marketing copy. Realistic rates are what you live on.

Cashback in stablecoins vs. cashback in tokens

The choice of cashback currency is the single biggest predictor of how much of the headline rate you keep. The trade-offs are worth working through carefully.

Volatility risk (when cashback in a token loses value)

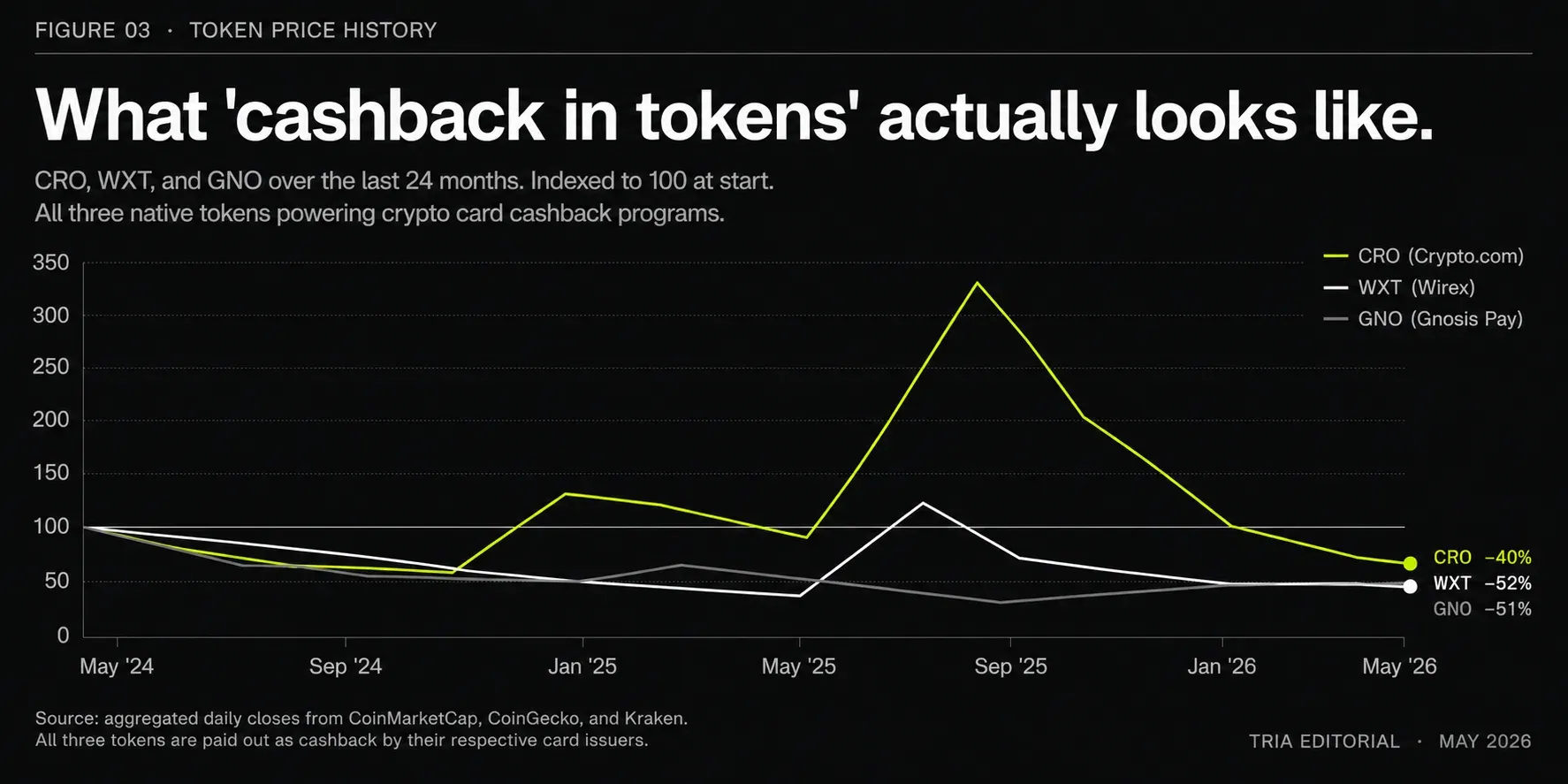

Cashback paid in an issuer’s native token carries that token’s full price risk. Three concrete examples from recent years:

- CRO (Crypto.com) has experienced multiple drawdowns greater than 50% from local highs.

- WXT (Wirex) has lost more than 80% of value at points relative to launch.

- GNO (Gnosis) has been more stable but still seen 30–40% drawdowns within 12-month windows.

A 5% cashback rate paid in a token that drops 40% is, in practical terms, a 3% cashback rate. The effective rate is whatever the token is worth at the moment you sell — not at the moment you earn.

Lockups and unstaking periods

Most issuer-token cashback programs include lockup conditions. Crypto.com’s tier system requires staking CRO for 6 months. Wirex applies vesting on Cryptoback. These lockups concentrate two risks: you can’t sell during a token drawdown, and you can’t reallocate the capital to a higher-yield use.

For users whose primary goal is predictable cash flow from card use, lockups are a meaningful drag. For users who specifically want exposure to the issuer’s token, lockups are part of the design.

Why stablecoin cashback is increasingly the default

The trend in self-custodial cards since 2024 has been toward stablecoin-denominated cashback. Three reasons drive it:

- Predictability — the headline rate equals the realized rate.

- Composability — stablecoin cashback can immediately earn yield, fund a swap, or back another card transaction without conversion friction.

- Compliance simplicity — issuers don’t have to navigate the regulatory questions that come with paying users in their own equity-adjacent token.

Tria, Coinbase, and several smaller self-custodial cards all default to stablecoins for this reason. Crypto.com, Wirex, and Gnosis Pay still pay in native tokens, partly because the tokenomics depend on the cashback flow as a demand sink.

How to maximize cashback without compromising self-custody

The cards with the highest headline cashback are mostly custodial. The cards that retain realized value tend to be self-custodial and stablecoin-denominated. The honest question is what you actually want from the card.

For low-to-mid monthly spend, no token holding

If you spend $1,000–$3,000/month and don’t want exposure to an issuer’s token, a self-custodial card with stablecoin cashback (Tria, Coinbase Card) gives you 2–6% realized cashback in a currency that holds its value. The Tria Card sits at the top of this group at up to 6%, and unlike custodial cards advertising 8% headlines, every percentage point of the Tria rate is what you actually take home — no volatility discount, no lockup.

For high monthly spend, willing to hold issuer tokens

If you spend $5,000+/month and you’ve already chosen to hold a meaningful amount of the issuer’s token (say, you’re long CRO independently), a tiered custodial card like Crypto.com can produce competitive realized cashback — but you’re effectively running two positions at once: the card and the token.

For DeFi-heavy users

If most of your activity is on-chain, Gnosis Pay’s Safe-account architecture lets cashback feed directly back into your DeFi stack with minimal friction. The 5% headline rate paid in GNO has more realized value for users who would hold GNO anyway.

The self-custody question

Custodial cards expose you to platform risk in addition to token risk. The 2022–2023 collapses (FTX, Celsius, BlockFi) reset what "safe" means in this category. Self-custodial cards remove that specific risk by keeping your balance in your own wallet until the moment of purchase. The realized cashback from a self-custodial card is paid into a balance you control — not into a custodian’s ledger you depend on.

Where Tria fits

The Tria Card pays up to 6% cashback in stablecoins, directly to your self-custodial Tria balance. Because there’s no token to stake and no lockup window, the rate you see is the rate you keep — no volatility discount, no waiting period. The underlying balance also earns up to 15% APY through Tria’s on-chain Earn product while it waits to be used. You keep your keys throughout. The card never takes custody.

In a category where the headline rate often hides 30–60% in volatility and lockup costs, the Tria Card is built around the opposite assumption: predictable, retainable cashback in a currency that holds its value, paid into a balance you actually control.

Set up a card-ready balance in the Tria app and start earning realized cashback in stablecoins.

Frequently asked questions

Is crypto card cashback taxable?

In most jurisdictions, crypto card cashback is treated as either a discount on purchase (not taxable) or as income (taxable at the fair market value when received). The treatment varies by country and by whether the cashback is paid in fiat, stablecoin, or a native token. Token cashback often creates a second taxable event when sold or converted. Check the rules in your jurisdiction or work with a crypto-aware tax professional.

What's the highest crypto card cashback rate available in 2026?

Headline rates of up to 8% exist on Crypto.com’s Obsidian tier (which requires staking ~$400,000 in CRO for 6 months) and Wirex’s top tier (which requires WXT staking with vesting). Realistic rates after accounting for tier requirements, payment currency, and lockups are typically much lower — often 1–3% for users without major token holdings. Tria offers up to 6% cashback paid in stablecoins with no token-staking requirement, which makes it the highest realized rate available to most users without committing capital to an issuer’s token.

Are crypto card cashback rates better than traditional credit card rates?

The headline numbers are usually higher on crypto cards (up to 8% vs. up to 5% for premium credit cards). The realized numbers are closer than the headlines suggest, because traditional cards pay cashback in dollars while many crypto cards pay in volatile tokens. For users on stablecoin-cashback crypto cards, the realized rate is typically competitive with or better than the equivalent traditional card.

Is custodial or self-custodial cashback better?

Self-custodial is structurally safer because your balance never sits with a third party. The cashback rates available on self-custodial cards are now competitive with custodial cards in 2026, which wasn’t true two years ago. The trade-off most users now face is between the highest tiers of custodial cards (which require capital lockup and accept platform risk) and self-custodial cards (which pay slightly lower headline rates but in retainable currencies, with no platform risk).

Can crypto card cashback compound while you wait to spend it?

On self-custodial real-time cards (Tria, Gnosis Pay), the underlying balance can earn on-chain yield while it waits to be used. Cashback paid into that balance starts compounding immediately. On custodial top-up cards, the balance is held by the issuer in fiat or stablecoins and typically doesn’t earn yield. The compounding effect adds 1–3% per year on top of the headline cashback rate for active users.